OPINION: ONE of the many accepted truisms in real estate is properties with a long WALE (weighted average lease expiry) tend to be lower risk.

The rationale is that during times of economic disruption, long-term in place contracted leases ensure a property’s ability to maintain cashflow, and presumably retain value.

But is that true?

In this article we analyse the data from the US REIT industry during the past two (very different) economic disruptions – the great financial crisis (2008-2009) and the great virus crisis (2020-2021) – and determine whether long WALE really is low risk.

What the data tells us

To test the narrative, we collected data from the US REIT industry across several sectors for the last two significant economic dislocations: the great financial crisis (2008-2009) and the great virus crisis (2020-2021). Then we grouped the sectors into two sub-groups:

Short lease duration (short WALE) – including residential, storage, lodging, healthcare (typically 0-1 year leases)

Long lease duration (long WALE) – including retail, office, industrial and triple net leasing / diversified (typically 5-10 year leases)

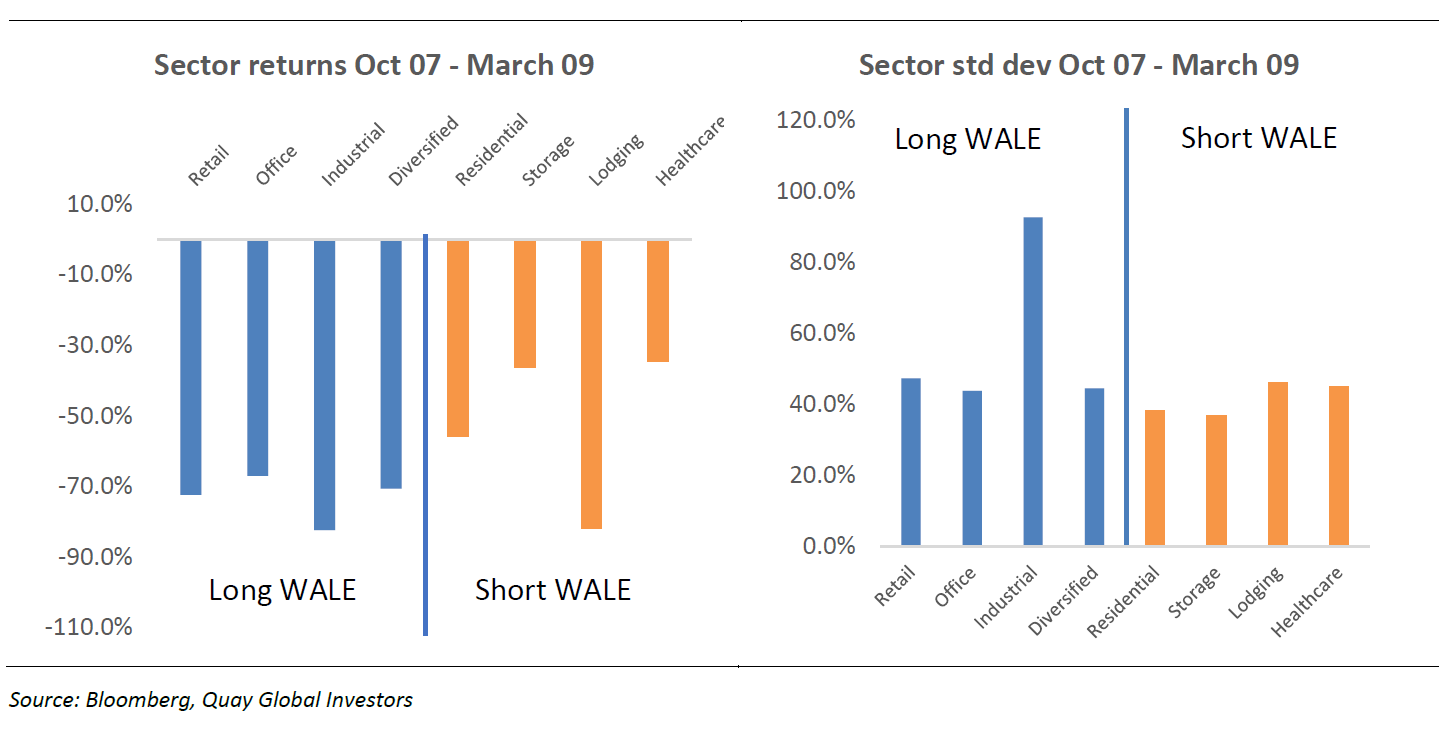

The following charts highlight the results for each sector during the great financial crisis, measuring both return and standard deviation (a proxy for risk). The colours of the bars reflect long WALE (blue) and short WALE (orange). The data was measured peak-to-trough for both series.

The immediate observation is there does not seem to be much difference in returns between long and short WALE – although if we are removing lodging, short duration appears to perform better. In terms of standard deviation (right chart), short WALE performed better. However, after excluding industrial, the risk appears similar.

In summary, being long WALE probably did not help much during the financial crisis – either for return or for risk.

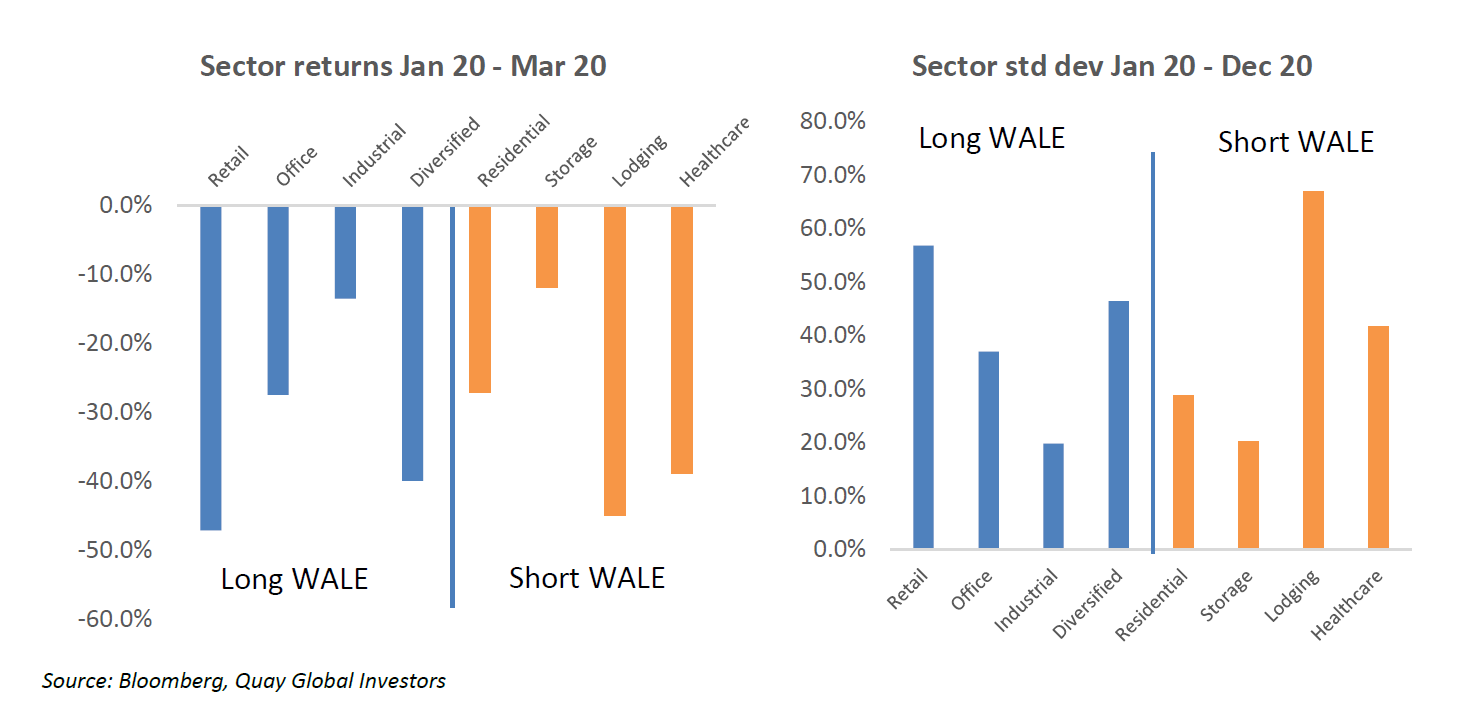

Next are the results for the great virus (COVID) crisis. The data was again measured peak-to-trough – however, for standard deviation we used 12 months for the COVID period to ensure we had enough monthly data and to capture the volatility around the virus and the vaccine.

The data during the COVID crisis paints a similar picture, although with some interesting variations. Again, being long WALE does not appear to either help or hinder the returns or the standard deviation during the crisis. However, industrial property performed significantly better during COVID in terms of return and risk compared to the financial crisis. Conversely, healthcare (a star performer during the GFC) suffered disproportionately during COVID.

Why is there limited capital protection from long WALE assets?

One could argue that assessing equity risk and return grouped by WALE is fraught with distortions – as management decisions, operating and financial leverage all impact equity returns – and we agree! There are so many other important factors that drive equity returns than WALE. We believe focusing on the other qualities of companies to be more fruitful.

In this respect, we remind our readers of our overall real estate philosophy – that is, the best way to manage risk is to buy value (below replacement cost where appropriate), buy quality (companies with higher barriers and high return on capital), buy low leverage, and bias sectors benefiting from some cyclical or secular tailwind.

When thinking about risk, we never think about WALE. In fact, since inception through to today, Quay’s portfolio tends to be very low on lease duration. Self-storage, single family housing, senior housing, apartments, manufactured housing and student accommodation (all with leases less than 1 year) historically account for ~60% of the portfolio. Notably, over this timeframe we have generally been underweight longer duration asset classes (office and industrial).

Despite our short portfolio WALE, since inception (July 2014) Quay’s concentrated 20-30 stock portfolio standard deviation of returns has been 15.3%, compared to 15.3% for the +300 stock FSTE/EPRA NAREIT global index. Why?

Notwithstanding the points made above about buying property companies vs actual assets, we believe the idea that long WALE equals low risk can be challenged on a number of fronts.

- Most real estate valuers and investors deeply understand the issue of reversion – this is the measure of how ‘out of the market’ current lease rates are compared to market. Good investors and valuers price this reversion into their valuation well before leases expire.

- Large tenants with long leases are a natural target for developers seeking to find an anchor tenant for new developments – usually a pre-requisite for funding. The long lead time to build (say, office) allows developers to target tenants with still-reasonable lease duration.

- Very long leases prevent landlords from managing leasing risk proactively. Few tenants wish to discuss new lease terms with +5 years still remaining.

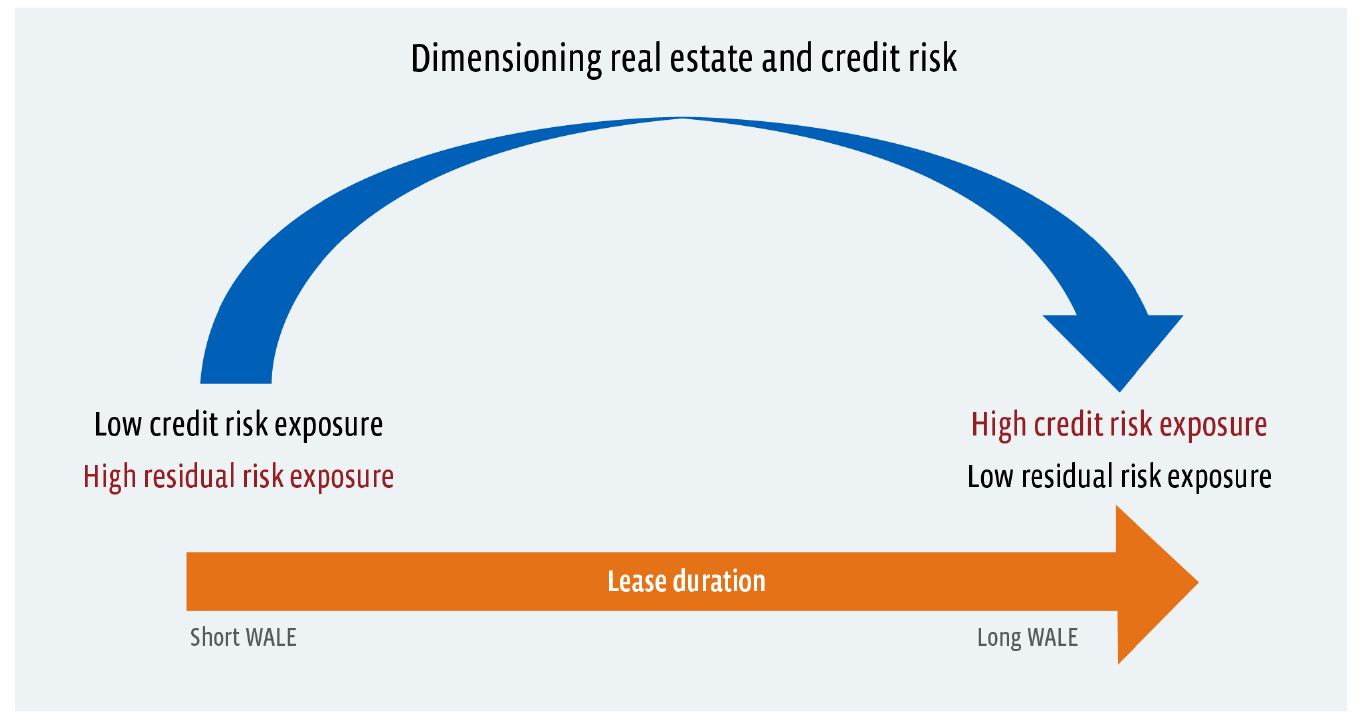

- Very long leases (WALE) alter the nature of the investment from a classic real estate exposure (short leases) to a credit exposure (long leases). This is because with long leases most of the ‘net present value’ is embedded in the lease rather than the end value (residual).

This final point is worth discussing in more detail. The diagram below conceptually shows the changing nature of real estate as lease duration increases. Advocates of long WALE argue the security of income from long leases protects investor cashflows over the cycle and therefore carries less risk. And having credit risk during times of distress is preferable to residual risk.

While it may sound reasonable to have credit risk rather than residual risk during a downturn, one aspect always lost on real estate investors – and never lost on bankers – is that credit is dynamic. For example, a 2020 study by Standard and Poors found that between 1981 and 2020, 51% of investment grade credit (BBB) was non-investment grade or unrated after ten years. Also, almost a third (32%) of AA rated credit became non-investment grade or not rated over the same timeframe[1].

The lesson for long WALE investors is: the credit you begin with may not be the credit you end with, and therefore your residual risk may be greater than you think.

All of which seems to be verified by the data.

Concluding thoughts

At Quay, we manage relatively concentrated portfolios (historically 20-30 securities) and as such we need to ensure we manage risk as well as generate acceptable total returns. We fundamentally believe the best way to manage risk is to intensively understand and research our investees, which is much easier to accomplish with a concentrated portfolio. Along with our usual risk mitigants listed above, we also avoid heavy capital recycling businesses (property developers) and businesses with lumpy returns (real estate managers).

What we do not do is spend much time thinking about average lease duration (WALE). The data and our track record suggest we are right to do so.

By Chris Bedingfield, Principal & Portfolio Manager, Quay Global Investors.*

Chris has over 30 years of experience working as a real estate specialist with a background in investment banking, equities research and investment management. He is a co-founder of Quay Global Investors, and co-launched the Quay Global Real Estate Fund in 2014. The Fund has since won numerous awards, including the 4x winner of the Global Property Securities category at the Money Management Fund Manager of the Year Awards in 2018, 2019, 2020 and 2021.

Chris’s current role includes portfolio management, stock and sector analysis, and he often publishes white papers covering an array of macroeconomic and global real estate themes. He has been a regular contributor and commentator on TV business news programs (including Sky Business/Your Money/AusBiz), regularly writes articles for national publications, and is frequently quoted in the media.

Chris holds a Bachelor of Business degree from UTS, with majors in Accounting, Finance and Economics. He was awarded the Securities Institute Diploma in 1994.

Prior to co-founding Quay, Chris was a senior member in the Real Estate Investment Banking group at Credit Suisse in Sydney and previously Head of Real Estate Investment Banking Asia at Deutsche Bank. In prior roles, he led real estate equities research teams at Deutsche Bank, HSBC James Capel and ANZ McCaughan where he was a consistently ranked top 3 research analyst for listed property.

He is experienced in equity and equity-linked capital markets transactions, M&A and debt issuance, with direct involvement in numerous cross border real estate transactions between Australia and the USA, Europe, Japan, UK, Brazil and Singapore.