OPINION: FOR investors and operators alike, the phrase ‘traditional retail’ currently invokes feelings of uncertainty and dread, and there is a level of panic associated with the demise of brick and mortar retail. But is the fear of the so-called ‘retail apocalypse’ warranted?

Not all retail is created equal

The retail landscape varies dramatically from country to country. The United Kingdom is the home of high street retail, where the United States is the land of not only the free, but also the shopping mall and has more shopping space per person than anywhere else in the world.

Australia has traditionally been a mix of shopping centres, big box retail (think Ikea) and everything in between, while just about every European country has a different story to tell.

What is consistent, however, is that the retail landscape at present, wherever you may be, is very much a case of adapt or perish. A primary driver of this outlook is the rise of e-commerce, which has disrupted many traditional retailers. As such, the industry has reached a point of no return, where longstanding beliefs are no longer a ticket to success.

Adaptation to quickly changing consumer behaviours is not necessarily easy for retailers, but is paramount in order to attract and retain customers. For those who can adapt, there has arguably never been a better time to be a retailer, or investor – if you know where to look.

Despite sensationalist headlines about the ‘retail apocalypse’, consumers still go shopping. While run-of-the-mill discretionary goods spend is highly vulnerable to e-commerce and tightening household budgets, non-discretionary goods and experiential factors are still prominent. As such, brick and mortar stores, are still unmatched when it comes to creating a shopping experience.

The impact of e-commerce

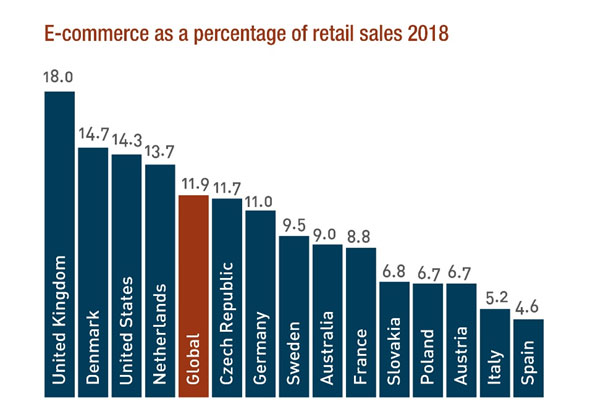

As online sales reach 11.9% of total retail sales globally, up from 7.4% in 2015 and forecast to reach 17.5% by 2021, there seems to be no sign of a reprieve for traditional operators who have not embraced the internet.

In terms of uptake for e-commerce purchase patterns, Australia lags behind about half of Europe, as well as the US, at 9% of total sales. The UK leads the pack at 18% of total retail sales, with the US sitting at just over 14%.

Between 2018 and 2023, e-commerce growth will be headlined by the United States, increasing 45.7% to US$735.4 billion per annum. France, 45.6% growth to US$71.9 billion p.a., Australia, 44.6% to US$26.9 billion p.a., and Germany, 35.6% to US$95.3 billion p.a., follow closely. The UK is anticipated to grow by less, 31.3%, to US$113.6 billion a year, but this is from a high base.

Online behemoths such as Amazon, who accounted for 40% of the United States’ online retail in 2018, continue to change the way in which consumers buy goods. The widely-held position is that this is to the detriment of traditional stores. This is evident through the demise, or seemingly impending demise of a number of big-name chains, such as Barneys New York recently filing for bankruptcy, David Jones’ owners writing down the department store’s value by $437 million, and two UK high street stalwarts, Boots and Mark & Spencer, announcing plans to close more than 300 stores between them.

The waning wealth effect

Coupled with e-commerce and cost of living pressures, the waning wealth effect also continues to impact retail investment decisions. These forces are altering consumer shopping behaviours, what they spend money on, and ultimately the performance of different retail subtypes.

Tightening of household budgets means consumers are ringfencing their non-discretionary spend while reducing their discretionary spend to the detriment of department and big box stores, as well as High Street retail.

Rental costs

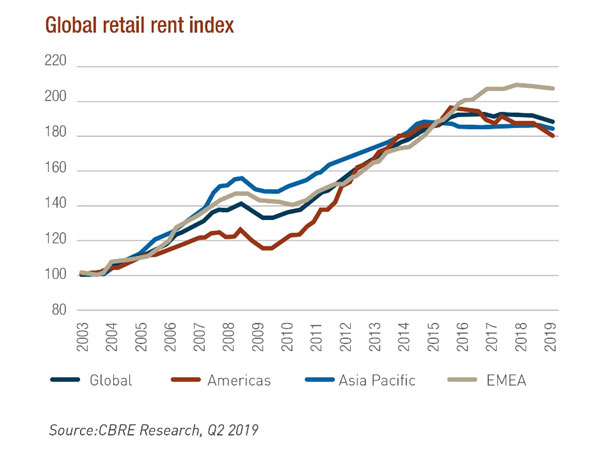

Retail rents have also begun to plateau, with downward readjustments occurring in an attempt to save struggling brick and mortar stores. However, legacy players are encumbered by high rents (often fixed and escalating), high debt levels that need to be addressed and changing consumer tastes from a discerning and cost-conscious consumer.

Even though rental growth has begun to stall, this is off the back of decades-long growth. For example, the most expensive retail location on earth in 1998, East 57th Street in New York, cost approximately US$425 per square foot (US$4,575 per sqm). Fast forward to 2018, and Causeway Bay in Hong Kong took top honours for the sixth time, with a top rent of US$2,671 per square foot (US$28,750 per sqm) – a six-fold increase.

City Council researchers in New York reported that average Manhattan rents rose 44% to US$156 per square foot (US$1,679 per sqm) between 2006 and 2016. Across the East River, Brooklyn retail rents averaged at least US$100 per square foot (US$1,076 per sqm) in 15 neighbourhoods as of 2017, up from three a decade prior.

The UK High Street is in a similar predicament with landlords consistently increasing rents. Retailers were on the expansion trail in the noughties, blissfully unaware the impact of e-commerce would have just over a decade later.

Capital: Influx or in flux?

Global

Institutional investors appear disinterested in retail assets halfway through 2019. The global retail outlook remains very much the same as it did early in the year – a degree of uncertainty clouds the economic outlook. A slowdown in China has weakened growth in emerging markets and some export-focused economies like Japan and Germany. The possibility of a no-deal Brexit has also weakened sentiment, as have the prolonged trade tensions between Trump’s United States and China. Equity markets have mostly bounced back from the lows experienced towards the end of 2018, but volatility still remains.

The retail sector continues to adjust to structural shifts, as global investment volumes in H1 2019 fell 20% on H1 2018 figures. The biggest decline was felt across Europe, the Middle East and Africa (EMEA), with H1 volumes down 43% year-on-year. The US saw a 10% decrease in H1, but on the flipside, Asia Pacific (APAC) saw a 7% rise in transaction volume.

Europe

To 30 June this year, just under 400 deals each valued at €5 million or more were closed, a stark decline on the 651 deals of a similar size through H1 2016. In terms of volume, the 400 aforementioned deals totalled €12.7 billion, which is contextually low given the €36.9 billion dealt in H1 2015.

Further, firms raising capital for strategies including retail peaked at US$3.5 billion through the first half of the year, down significantly on the last couple of years.

Australia

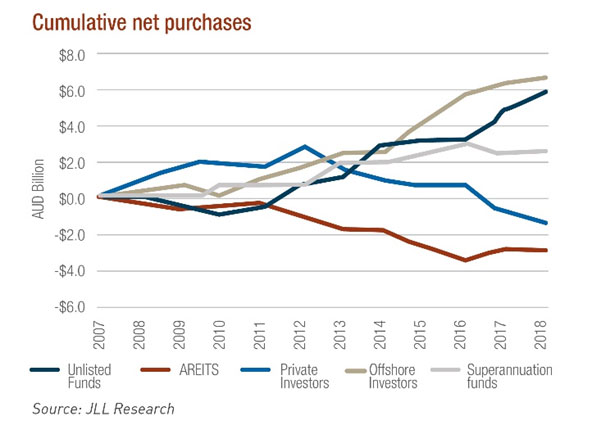

Retail transaction activity reached $8.1 billion in 2018, the third highest level on record. Unlisted funds dominated these acquisitions and it is anticipated the trend of transferring from listed to unlisted ownership will continue throughout 2019 as AREITs continue to refine their portfolios.

However, investors are proceeding with caution when it comes to retail fundamentals, particularly with regard to income stability and capital intensity.

United States

Marred by a spate of closures this year – approximately 7,500 of which were announced by major chains in the first half of 2019 alone – US retailers continue to be battered by high costs, competition from e-commerce and the debt burden carried from past leveraged buyouts.

Despite this, investors remain active. In the first quarter of 2019, US$11.1 billion in assets were traded, and despite a -4.9% year-on-year change, institutional investors are keen to deploy capital for well-located assets in primary or high-growth secondary markets.

What lies ahead?

Omni-channel retailing

Retailer success will depend significantly on a sound omni-channel strategy. Across most categories and price points, transactions are shifting online and retailers are using their store networks for customer acquisition, brand experience, online order fulfillment, returns and data gathering.

E-tailers, such as Amazon, are going one step further by adopting the ‘clicks-and-bricks’ trend, where previously online-only entities are opening physical stores – highlighting the need for an on-the-ground presence.

This makes sense, as a study conducted in Europe by Ipsos found 70% of consumers prefer to buy online with retailers who have a brick and mortar presence.

Experiential shopping

As shoppers are now able to buy almost any product, anywhere, shopping centres and malls, as well as brick and mortar retailers must therefore fulfil consumers’ desire for entertainment and experience, rather than the traditional procedure of purchasing and owning things.

Globally, leasing in malls and shopping centres will be dominated by food and beverage, cosmetics, lifestyle and experience-based offerings. Landlords of midmarket, mid-tier centres are repositioning to attract these types of tenants.

In the US, this is particularly easy given the sheer volume of vacancies caused by store closures. On the other side of the International Date Line, experiential factors remain a focus for APAC shopping centres, but a trend in co-working spaces in centre locations is also gaining prominence.

Another strategy is to seek operators that cater to the growing health and fitness-conscious consumer. This may include leasing space to a gym or fitness centre, as well as seeking health-focused food and beverage tenants, or even food and produce markets.

In APAC alone, growing consumer demand for experiential shopping is expected to see experience-based spending total US$825 billion between 2018 and 2030. Centres with established experiential retail models are proof of how successful they can be.

There is no shortage of opportunity for those who know where to look. Moving forward, in an almost oxymoronic way, retail will likely form a smaller part of the tenant mix, as non-retail facilities such as restaurants, childcare facilities, fitness and services become standard in many locations.

Traditional retail is therefore being resized, reinvented and reimagined. This is leading to retailer restructuring and shrinking store networks and the disruption is creating the inevitable opportunities for new operators and formats to emerge.

By Bobby Binning, Head of Property at Cromwell Property Group*

Property Reviewer on Australian Property Journal